The Treasury this week disclosed details of their plan to pump $1 trillion into the financial system by removing “Legacy Assets” from the balance sheets of banks. Wading through the multitude of documents and documents, I’m reminded of a remark by Michael Milken in a conversation with Charlie Rose on October 27, 2008 “Complexity is not innovation.”

Since its inception, the plan has been sold to Congress and the media as one with potential positive payoffs for the public coffers. To support this idea, proponents point to the experience of the Resolution Trust Company (RTC) in resolving the Savings and Loan (S&L) Crisis . Back then, RTC took over failing S&Ls – some of which were bankrupted by bad real estate loans made worse when they were forced to sell off below-investment grade bond assets – the by-now-well-known Junk Bonds

. Back then, RTC took over failing S&Ls – some of which were bankrupted by bad real estate loans made worse when they were forced to sell off below-investment grade bond assets – the by-now-well-known Junk Bonds .

.

Selling off today’s junk bonds will, I agree, clean up the balance sheets of the banks and make them more attractive to investors and depositors. But the investment in junk bonds now is not going to turn out like the investment in junk bonds then. For starters, the value of the junk bonds then declined as a result of the forced sell-off – Congress prohibited S&Ls from holding junk bonds on their balance sheets. When this supply was dumped on the market, the prices naturally dropped. Selling assets at depressed prices damaged a lot of S&Ls. RTC stepped in near the bottom of those prices to take control of the assets. When credit markets returned to normal, the prices of the junk bonds rose and the investments had positive returns.

Then, junk bonds paid extraordinary rates of return – 10 percentage points above Treasuries at the peak. At that time, a 30-year U.S. Treasury bond could be paying more than 18% interest.

Now, we are talking about junk bonds that we all know are junk – no matter fancy labels like “Legacy.” What rate of return could there be on a mortgage bond – no matter how you “slice-and-dice” it – created when mortgage interest rates were 5-6%? Add to that our knowledge of the problems underlying these assets and it is increasingly unlikely that there will be any positive payoff for taxpayers in this plan.

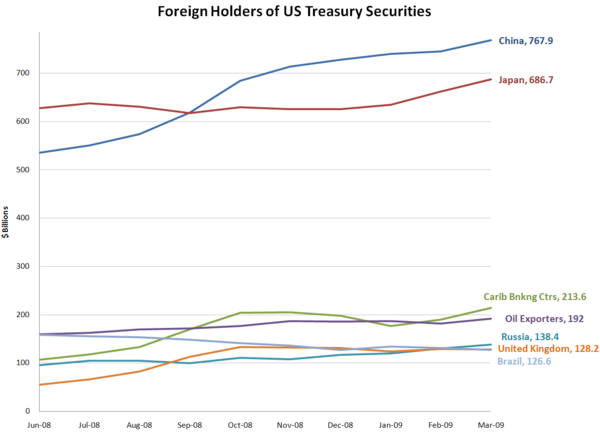

On March 25, 2009, Mirek Topolanek, President of the European Union, called the U.S. economic plan “the way to hell.” His concern is that we’ll have to finance these trillion dollar bailouts with borrowing and that will ultimately further undermine global financial markets. He’s right, of course. The public-private partnerships will finance the purchase of the “Legacy Assets” by issuing debt. That debt will be guaranteed by the Federal Deposit Insurance Corporation (FDIC), the same agency that guarantees our savings accounts at the local bank. Our guarantee is backed by the payment of insurance premiums to FDIC. The guarantee on the debt used to purchase Legacy Assets will be secured by the Legacy Assets – which will be rated by the same credit rating agencies that gave us triple-A rated subprime mortgage bonds in the first place. How can this possibly turn out well? I’m sure Treasury, Federal Reserve and FDIC have good intentions, but as EU President Topolanek says, they may all end up as pavement on “the way to hell.” As NYTimes columnist Paul Krugman said of the new plan, “What an awful mess.”