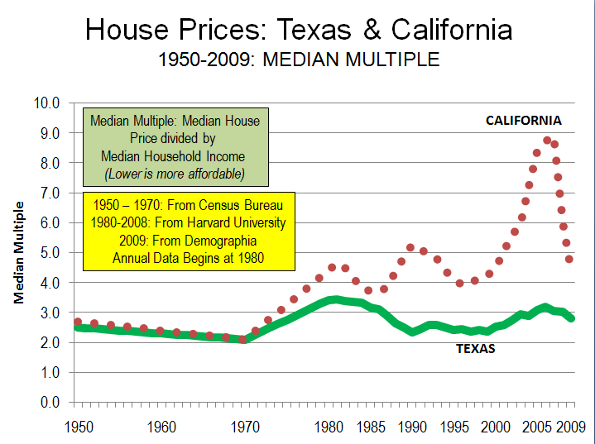

The first decade of the new millennium was particularly hard on the US economy. First, there was the recession that followed the attacks of 9/11. That was followed by the housing bust and the resulting Great Financial Crisis, which was the most severe economic decline since the Great Depression.

Per capita personal incomes in America’s major metropolitan areas vary widely. Moreover, the changes in per capita incomes from 2000 to 2009 have also varied. The differences are particularly obvious when average incomes are adjusted for metropolitan area Consumer Price Indexes. The US Bureau of Labor statistics produces a Consumer Price Index for nearly 30 metropolitan areas. Among these, 28 metropolitan areas are covered by these local Consumer Price Indexes.

While overall national inflation was approximately 25 percent between 2000 and 2009, the metropolitan area inflation indexes ranged from 16 percent in Phoenix to more than 32 percent in San Diego. Five additional metropolitan areas had 2000 to 2009 inflation of more than 30 percent, including Los Angeles, Riverside-San Bernardino, Miami, Tampa-St. Petersburg and San Diego. Four metropolitan areas experienced inflation of less than 20 percent, including Atlanta, Detroit and Cleveland and Phoenix.

Overall, the 28 metropolitan areas covered by metropolitan inflation indexes averaged a per capita income decrease of 0.1 percent, after adjustment for inflation. Increases were achieved in 18 metropolitan areas, while decreases occurred in 10. The overall average declines occurred because the steepest loss (19 percent in San Jose), was far outside the plus 10 percent to minus 8 percent range of the other 27 metropolitan areas (Table).

| Metropolitan Area: Per Capita Income | ||||

| Metropolitan Areas Covered by Metropolitan Consumer Price Indexes | ||||

| Inflation Adjusted | ||||

| Rank | Metropolitan Area |

2000 in 2009$

|

2009

|

Change

|

| 1 | Baltimore |

$ 43,729

|

$ 47,962

|

9.7%

|

| 2 | Pittsburgh |

$ 39,024

|

$ 42,216

|

8.2%

|

| 3 | Washington |

$ 53,753

|

$ 56,442

|

5.0%

|

| 4 | Philadelphia |

$ 43,572

|

$ 45,565

|

4.6%

|

| 5 | St. Louis |

$ 38,636

|

$ 40,342

|

4.4%

|

| 6 | Milwaukee |

$ 40,028

|

$ 41,696

|

4.2%

|

| 7 | Los Angeles |

$ 41,382

|

$ 42,818

|

3.5%

|

| 8 | Houston |

$ 42,232

|

$ 43,568

|

3.2%

|

| 9 | Cleveland |

$ 38,396

|

$ 39,348

|

2.5%

|

| 10 | Chicago |

$ 42,761

|

$ 43,727

|

2.3%

|

| 11 | Phoenix |

$ 33,594

|

$ 34,282

|

2.0%

|

| 12 | San Diego |

$ 44,812

|

$ 45,630

|

1.8%

|

| 13 | Kansas City |

$ 39,020

|

$ 39,619

|

1.5%

|

| 14 | New York |

$ 51,638

|

$ 52,375

|

1.4%

|

| 15 | Cincinnati |

$ 37,852

|

$ 38,168

|

0.8%

|

| 16 | Seattle |

$ 48,651

|

$ 48,976

|

0.7%

|

| 17 | Boston |

$ 53,396

|

$ 53,713

|

0.6%

|

| 18 | Minneapolis-St. Paul |

$ 45,690

|

$ 45,750

|

0.1%

|

| 19 | Denver |

$ 46,205

|

$ 45,982

|

-0.5%

|

| 20 | Miami-West Pallm Beach |

$ 41,937

|

$ 41,352

|

-1.4%

|

| 21 | Riverside-San Bernardino |

$ 30,600

|

$ 29,930

|

-2.2%

|

| 22 | Portland |

$ 39,703

|

$ 38,728

|

-2.5%

|

| 23 | Tampa-St. Petersburg |

$ 38,048

|

$ 36,780

|

-3.3%

|

| 24 | San Francico |

$ 61,831

|

$ 59,696

|

-3.5%

|

| 25 | Dallas-Fort Worth |

$ 41,575

|

$ 39,514

|

-5.0%

|

| 26 | Detroit |

$ 40,412

|

$ 37,541

|

-7.1%

|

| 27 | Atlanta |

$ 39,775

|

$ 36,482

|

-8.3%

|

| 28 | San Jose |

$ 68,185

|

$ 55,404

|

-18.7%

|

| Unweighted Average |

$ 43,801

|

$ 43,700

|

-0.2%

|

|

The Top Ten: The strongest per capita personal income growth between 2000 and 2009 was in Baltimore, which had an inflation adjusted increase of 9.7 percent. This strong performance is not surprising due to Baltimore’s proximity to Washington and the federal government’s high paying jobs. It also receives spillover lucrative employment from federal contracts to health, defense and security companies. In fact, Baltimore did better than Washington. Washington, which extends from the District of Columbia and into Maryland, Virginia and West Virginia. Not that DC did badly; it boasted the third highest income growth, and 5.0 percent.

However, perhaps the biggest surprise is the metropolitan area that slipped into the number two position between Baltimore and Washington. The Pittsburgh metropolitan area, which may have faced the most severe economic challenges of any major metropolitan area over the past 40 years, achieved per capita personal income growth of 8.2 percent. The Pittsburgh gain is all the more significant in view of the local financing difficulties which placed the city of Pittsburgh in the near equivalent of bankruptcy under Pennsylvania’s Act 47. However, as is the case in on number of metropolitan areas, the central city has become much less dominant and no longer seals the fate of the larger metropolitan area. Today, the city of Pittsburgh accounts for only 15 percent of the metropolitan area population.

Philadelphia, the other long troubled region across the state, constitutes another surprise. Philadelphia placed fourth in per capita income growth at 4.6 percent only slightly behind Washington. The Philadelphia metropolitan area borders on that of Baltimore, stretching from Pennsylvania into New Jersey, Delaware and Maryland. Together with Washington and Baltimore, Philadelphia anchors the northern end of a corridor of comparative prosperity.

Four of the next six positions are occupied by Midwest metropolitan areas. This may be unexpected because of the significant job losses sustained in this area since 2000. St. Louis, which stretches from Missouri into Illinois, ranked fifth in per capita income growth, at 4.4 percent. Milwaukee ranked sixth in its per capita income growth at 4.2 percent. Cleveland ranked ninth with per capita income growth of 2.5 percent, while Chicago placed 10th, with a gain of 2.3 percent in per capita personal income.

Los Angeles was the only metropolitan area in the West to place in the top 10 in per capita income growth. Los Angeles ranked seventh growth of 3.5 percent. Houston replaced eighth with personal income growth of 3.2 percent.

Overall, the East and Midwest captured six of the top ten income positions, while the South and West occupied four of the top ten positions.

The Bottom 10: If the top 10 contained surprises, the bottom 10 could be even more surprising. Last place (28th) was occupied by San Jose, which experienced a stunning 18.7 percent decline in per capita inflation adjusted income between 2000 and 2009. This income loss is more than double that of the second-worst performing metropolitan area and more than triples that of all but two other metropolitan areas.

The second worst position (27th) also contained a surprise, in Atlanta, which has enjoyed decades of unbridled growth. Yet, Atlanta experienced a per capita income loss of 8.3 percent. There was no surprise in the third to the last ranking (26th) of Detroit, with its automobile industry employment losses and the physical deterioration of its central city, which may be unprecedented in modern peace-time. Per capita incomes declined 7.1 percent in Detroit.

Dallas-Fort Worth, which has also experienced strong growth in the past, posted a surprising fourth worst, with a per capita income decline of 5.0 percent. San Francisco, which has now replaced San Jose as the metropolitan area with the highest per capita income, ranked fifth worst and experienced a decline of 3.5 percent.

All of the remaining bottom 10 positions were occupied by metropolitan areas that have developed a reputation for strong growth. Tampa St. Petersburg ranked 6th worst, with a per capita income loss of 3.3 percent. Portland (Oregon) ranked 7th worst with a personal income loss of 2.5 percent. Riverside San Bernardino, with the lowest per capita income ranking out of the 28 metropolitan areas, ranked 8th worst with a per capita income drop of 2.2 percent.

The Miami (to West Palm Beach) metropolitan area ranked 9th in personal income growth with a loss of 1.4 percent from 2000 to 2009, while Denver topped out the bottom 10, ranking, with a per capita income loss of 0.5 percent

Overall, the South and the West captured nine of the bottom ten positions, while only one Midwestern metropolitan area, Detroit, broke into the bottom ten.

Of course, the 2000s certainly were an unusual time. But it does suggest that the dogma about the geography of regional prosperity needs to be challenged and perhaps thoroughly revised.

Photo: Pittsburgh: Second Fastest Growing Income per Capita 2000-2009 (photo by author)

Wendell Cox is a Visiting Professor, Conservatoire National des Arts et Metiers, Paris and the author of “War on the Dream: How Anti-Sprawl Policy Threatens the Quality of Life”