In a previous post we looked at which states have been most competitive in terms of job creation since the recession.

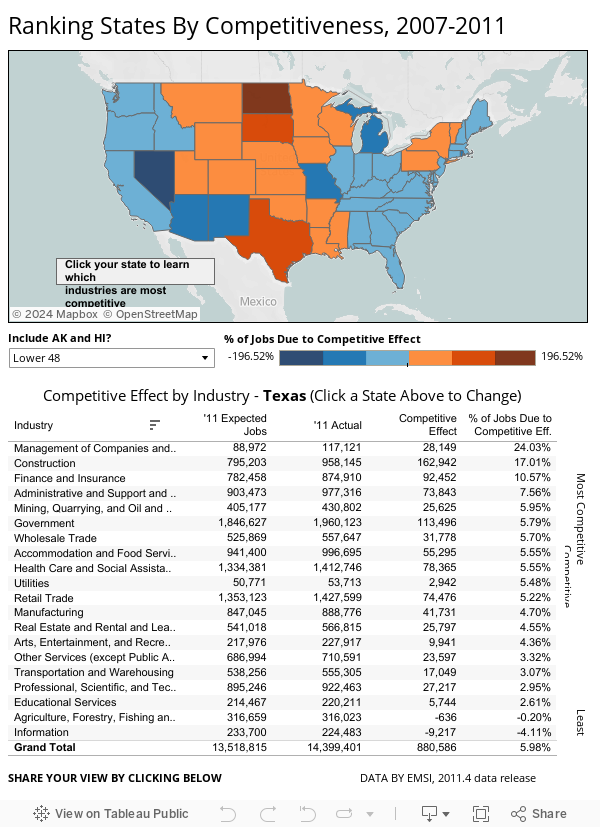

In this post we teamed up with our friends at Tableau Software to produce the following interactive graphic, which details individual industries that are driving states to be more (or less) competitive. The graphic breaks down the performance of the 20 major sectors in every state in the contiguous US (plus Hawaii and Alaska) in terms of expected and actual job change from 2007-2011. Further explanation of the analysis is below.

Rundown on the data

We used shift share, a standard economic analysis method that reveals if overall job growth is explained primarily by national economic trends and industry growth or unique regional factors. Shift share analysis, which can also be referred to as “regional competitiveness analysis,” helps us distinguish between growth that is primarily based on big national forces (the proverbial “rising tide lifts all boats” analogy) vs. local competitive advantages.

To generate our ranking, we summed the overall competitive effect for each broad 2-digit industry sector by state (e.g., agriculture, manufacturing, health care, construction, etc.) and added them together to yield a single statewide number that indicates the overall competitiveness of the economy as compared to total economy. We calculate the competitive effect by subtracting the expected jobs (the number of jobs expected for each state based on national economic trends) from the total jobs. The difference between the total and expected is the competitive effect. If the competitive effect is positive, then the industries within the state have exceeded expectations and created more jobs than national trends would have suggested. Those industries are therefore gaining a greater share of the total jobs being created. If the competitive effect is negative, then the industries are not gaining jobs as fast as what we would expect given national trends. In this case the state is losing a greater share of the total jobs being created.

Observations On Most Competitive

The big thing that stands out is that most of the competitive states tend to be in the middle of the country. This is tied to the growth in the oil and gas sector, yes, but in most cases better-than-expected performance in construction, government, and other miscellany sectors. In Alaska, North Dakota, and Nebraska, smaller states in terms of population and jobs, manufacturing, transportation, and construction are some of the most competitive industries. Louisiana also fares quite well in healthcare and accommodation & food services.

Observations On Least Competitive

For states that rank toward the bottom, the housing bust and subsequent construction downturn is the biggest culprit. For instance, in Nevada, which is last on the list, construction is nearly 50,000 jobs below what would be expected given national and industry trends. Florida, a much more populous state, is more than 130,000 jobs below what would be expected. For states like Michigan, Ohio, and Indiana, the poor performance in manufacturing and government weighed heavily in our ranking.

Here is the original graphic that show the comparison between states.

Please check out the graphic and let us know if you have any questions. Email Rob Sentz (rob@economicmodeling.com) or hit us via Twitter @DesktopEcon. Data and analysis comes from Analyst, EMSI’s web-based labor market analysis tool.